Stay informed with expert perspectives, industry trends, and practical strategies from the Trace Consultants team. Our insights explore the challenges and opportunities shaping supply chains today, helping you make confident, informed decisions.

Sustainability Reporting in Australia: Are You Ready for What's Coming?

Sustainability reporting is now mandatory for many Australian organisations. Under AASB S2, organisations must disclose climate-related risks and opportunities, including Scope 3 emissions. This guide covers what the requirements mean in practice and how to turn compliance into a genuine competitive advantage.

Sustainability reporting in Australia is now mandatory for many organisations. Under AASB S2 Climate-Related Disclosures, Australian organisations are required to report on climate-related risks and opportunities, including mandatory reporting of Scope 3 emissions. Driven by consumer demand and regulatory pressure, sustainability is no longer voluntary target-setting. The question for most organisations right now is not whether these requirements apply to them. It is whether they are ready.

Assess how ready you are

Before responding to new sustainability reporting obligations, it is worth being honest about where your organisation currently stands. Six questions worth asking:

Do you know your reporting group, deadlines, and which mandatory obligations apply to you?

Do you have the right internal capability to meet AASB S2 requirements?

Have you identified the climate-related risks and opportunities that could impact your strategy, operations, or financial performance?

Which categories of suppliers contribute most significantly to your climate-related risks or opportunities?

Do you have reliable Scope 1, 2, and (material) Scope 3 emissions data?

Do you have the systems needed to collect, verify, store, and report emissions information consistently?

If the answers to several of these are unclear, you are not alone. Many Australian organisations are still working through these foundations.

Benefits of strategic sustainability reporting

Sustainability reporting is often framed purely as a compliance burden. Organisations that treat these requirements as a foundation for broader improvement tend to unlock four tangible benefits:

Cost reductions

Identifying inefficiencies and reducing costs through sustainability frameworks.

Operational improvements

Streamlining operations with data-driven sustainability processes.

Stakeholder trust

Strengthening stakeholder confidence through transparent ESG disclosures.

Innovation

Uncovering new opportunities by embedding sustainability into strategy.

The organisations that move confidently from disclosure and reporting to long-term value creation are the ones that treat these requirements as a starting point, not a finish line.

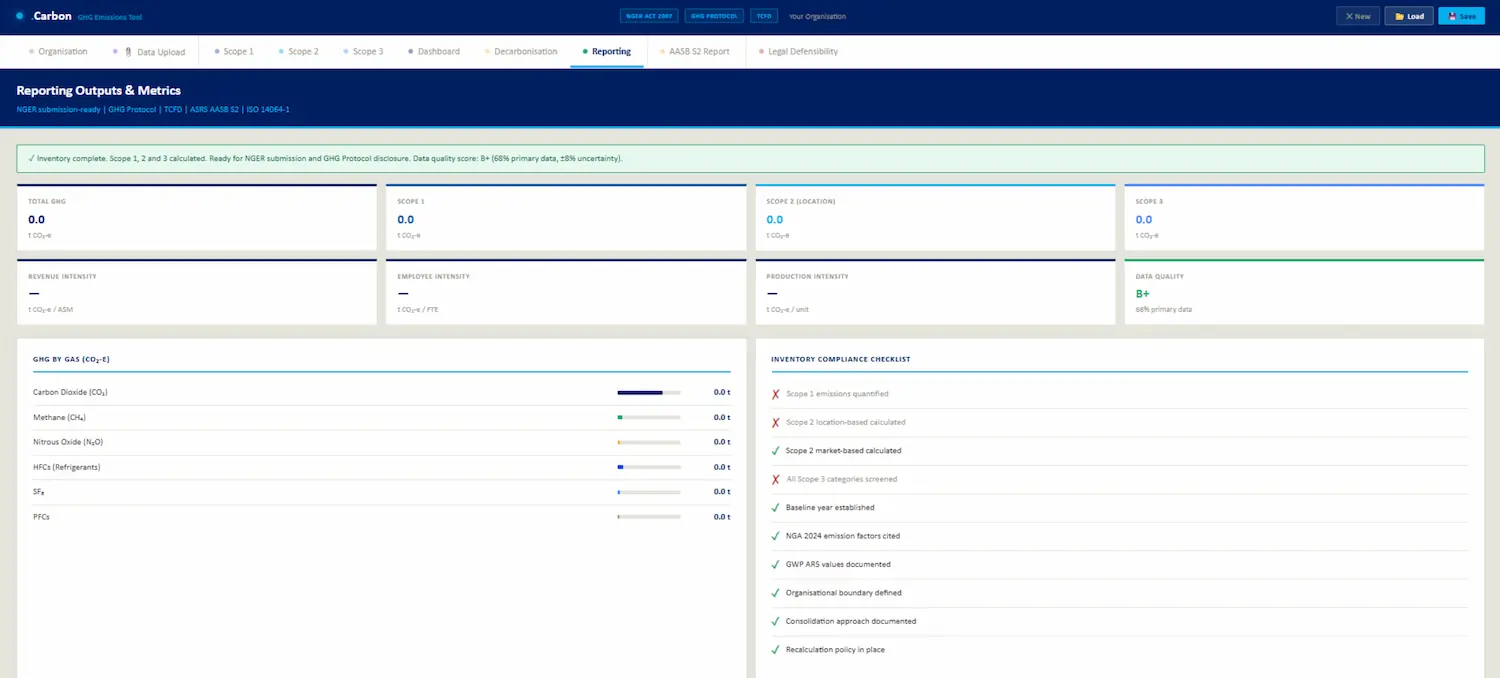

To help organisations navigate this complexity, Trace has developed .Carbon, an integrated GHG emissions calculator and sustainability disclosure tool designed to help organisations better understand their emissions profile in a simplified manner.

Screenshot of the .Carbon dashboard

.Carbon enables organisations to:

Quantify Scope 1, 2, and 3 greenhouse gas emissions

Model decarbonisation scenarios and maintain an abatement register

Scaffold an AASB S2-aligned four-pillar disclosure report

Track progress against targets

The tool is built for regulatory alignment across six frameworks: NGER Act 2007, NGA Factors 2024, GHG Protocol, ISO 14064-1, SBTi Corporate, and ASIC RG 228. Its reporting tab produces submission-ready metrics and compliance outputs across eight regulatory and voluntary frameworks.

Case study: Crown

Trace worked with Crown to deliver two sustainability initiatives with measurable outcomes. We supported the implementation of a Central Energy Plant with the aim of a 68% reduction in CO2 emissions per annum through gas and electricity reductions, unlocking both operational and financial benefits including $8.3 million in savings per annum.

We also created a web-based Delta T Quick Assessment and Calculator for Crown's portfolio companies and buildings, tracking energy savings, emissions reductions, and associated annual cost savings.

Sustainability reporting doesn't have to be overwhelming. As one of Australia's leading supply chain consultancies with proven expertise in creating sustainable results, Trace can guide organisations from supply chain mapping and risk assessment through to emission calculation, reporting, and decarbonisation initiatives.

We work alongside your team to develop sustainability strategies that use requirements as a foundation for identifying efficiencies, strengthening stakeholder relationships, and building a measurable, lasting competitive advantage.

AASB S2 is Australia's mandatory climate-related financial disclosure standard, aligned with the International Sustainability Standards Board's IFRS S2. It requires organisations to disclose climate-related risks and opportunities across four pillars: governance, strategy, risk management, and metrics and targets.

Who does AASB S2 apply to?

AASB S2 applies to large Australian entities in phases. Group 1 entities, those with two of the following: 500 or more employees, $1 billion or more in consolidated gross assets, or $500 million or more in consolidated revenue, were required to report from 1 January 2025. Groups 2 and 3 follow in subsequent years.

What is Scope 3 emissions reporting?

Scope 3 emissions are indirect greenhouse gas emissions that occur across an organisation's value chain, including upstream supplier emissions and downstream customer use of products. Under AASB S2, material Scope 3 emissions must be measured and disclosed, making supply chain emissions data a critical input for compliance.

How can Trace help with sustainability reporting?

Trace helps Australian organisations navigate sustainability reporting from end to end, including supply chain mapping, emissions calculation, AASB S2 disclosure preparation, and decarbonisation strategy. Trace has also developed .Carbon, an integrated GHG emissions calculator and sustainability disclosure tool built for regulatory alignment across six frameworks.

Sustainability

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Procurement Operating Models: How to Move From Cost Centre to Strategic Function

Most organisations say they want strategic procurement. Few have built the operating model to deliver it.

The gap is visible in how procurement teams spend their time. If the majority of effort goes into processing purchase orders, chasing approvals, managing contracts after they have been signed, and responding to urgent requests from the business, then the function is operating transactionally regardless of what the org chart says. Strategic procurement, the kind that actively drives cost reduction, manages supply risk, builds supplier capability, and creates competitive advantage, requires a deliberately designed operating model that aligns people, processes, governance, and technology around value creation rather than transaction processing.

This article provides a practical framework for designing a procurement operating model that works in an Australian context. It covers the common structural choices, the maturity journey, the capability requirements, and the implementation approach that distinguishes successful procurement transformations from the ones that stall after the strategy deck is presented.

What a Procurement Operating Model Actually Is

An operating model is not an org chart. It is the integrated design of how a function delivers its outcomes. For procurement, it covers five interconnected elements:

Structure defines where procurement sits in the organisation, how it is organised internally (by category, by business unit, by geography, or some combination), and where decision rights sit. The three dominant structural models are centralised, decentralised, and centre-led.

Process defines how work flows through the function: from demand identification and sourcing strategy through to contract execution, supplier management, and performance reporting. The maturity and standardisation of these processes determines whether procurement operates consistently or ad hoc.

People and capability defines what skills the function needs, at what levels, and how those skills are developed and maintained. The difference between a transactional and a strategic procurement function is almost entirely a capability question.

Governance defines how decisions are made, who has authority to commit spend at each threshold, how procurement interacts with finance and the business, and how performance is measured and reported.

Technology and data defines the systems that enable procurement activity: e-procurement platforms, contract management tools, spend analytics, supplier portals, and the data infrastructure that underpins visibility and decision-making.

A well-designed operating model integrates these five elements so they reinforce each other. A poorly designed one, or one that has evolved organically without deliberate design, creates friction, duplication, and gaps that the team spends its energy working around rather than delivering value through.

The Structural Choice: Centralised, Decentralised, or Centre-Led

The structural question is where most organisations start, and where many get stuck.

Centralised procurement consolidates all procurement activity into a single function that manages sourcing, contracting, and supplier management on behalf of the entire organisation. The advantages are clear: spend visibility, leverage through aggregation, consistent process, and strong governance. The disadvantage is equally clear: distance from the business. A centralised team that does not understand the operational context of what it is buying will make technically correct but practically poor sourcing decisions. Centralised models work best in organisations with relatively homogeneous spend categories and a strong mandate from the executive to consolidate.

Decentralised procurement distributes procurement responsibility to individual business units, sites, or functions. Each unit buys what it needs, often with its own processes and supplier relationships. The advantages are responsiveness and local knowledge. The disadvantages are fragmented spend, limited leverage, inconsistent process, poor visibility, and compliance risk. In practice, many organisations that describe themselves as having "no procurement function" are actually operating a decentralised model by default: everyone is buying, nobody is coordinating.

Centre-led procurement is the model most Australian organisations should be targeting. It centralises strategic activities (category strategy, major sourcing events, contract frameworks, supplier management standards, spend analytics) while delegating operational procurement (call-offs against established contracts, low-value purchasing, local supplier engagement) to the business. The centre sets the rules, builds the tools, and manages the categories. The business operates within that framework with appropriate autonomy.

The centre-led model works because it resolves the fundamental tension between leverage and responsiveness. It captures the aggregation benefits of centralisation while preserving the operational agility of decentralisation. But it requires clear role definitions, strong governance, and a level of trust between the centre and the business that does not exist by default. It has to be built.

The Maturity Journey: Where Most Organisations Get Stuck

Procurement maturity models typically describe four or five stages, from ad hoc purchasing through to strategic value creation. The labels vary, but the pattern is consistent:

Stage 1: Reactive. No formal procurement function. Buying happens across the organisation without coordination. No spend visibility. No category management. No supplier strategy. This is more common than it should be, particularly in mid-sized organisations and in sectors like hospitality, health, and property where procurement has historically been an administrative rather than a strategic function.

Stage 2: Tactical. A procurement team exists and manages major purchases, but operates primarily as a processing function. The team runs tenders, negotiates contracts, and manages compliance, but has limited influence over what gets bought, when, or from whom. Spend analytics are basic or manual. Supplier management is reactive: the team engages with suppliers when there is a problem, not proactively to drive performance.

Stage 3: Structured. Category management is in place for major spend areas. Sourcing strategies exist and are executed through a defined process. Spend visibility is reasonable. The procurement team has a seat at the table for major investment and operational decisions, though influence varies by category and by the personal credibility of the procurement lead. This is where most "good" procurement functions in Australia currently sit.

Stage 4: Strategic. Procurement is fully integrated into business planning. Category strategies align with organisational strategy. Supplier relationships are managed as assets, with structured performance management, development programmes, and innovation partnerships. Total cost of ownership drives sourcing decisions, not just unit price. The CPO reports to the CEO or CFO and is a genuine member of the leadership team. Relatively few Australian organisations have reached this stage consistently across all categories.

The gap between Stage 2 and Stage 3 is where most procurement transformations stall. The reason is almost always capability. Building category management capability, developing should-cost models, implementing structured supplier management, and shifting the team's mindset from processing to analysing requires investment in people that many organisations are reluctant to make. They want the outcomes of Stage 3 or 4 procurement with the headcount and skill profile of Stage 2. That does not work.

Capability: The Make-or-Break Factor

The single most important determinant of procurement operating model effectiveness is the capability of the people in the function. Process, governance, and technology all matter, but they are enablers. Without the right people, doing the right work, at the right level of skill, no operating model will deliver its intended outcomes.

The capability requirements shift as the operating model matures. At Stage 1 and 2, the dominant skills are administrative: order processing, contract administration, compliance checking. At Stage 3 and 4, the dominant skills are analytical and commercial: market analysis, should-cost modelling, negotiation strategy, supplier relationship management, stakeholder engagement, and category strategy development.

This creates a transition challenge. The people who are excellent at Stage 2 work are not necessarily the people who will excel at Stage 3 work. The skills are genuinely different. Some team members will develop into the new model with coaching and training. Others will not. Managing that transition with honesty and respect, while simultaneously delivering on the promise of the new model, is one of the hardest aspects of procurement transformation.

The practical approach is to invest in three areas simultaneously. First, recruit for the capability you need at the senior end: experienced category managers who have done the work before and can demonstrate what "good" looks like to the rest of the team. Second, develop existing team members through structured training, mentoring, and exposure to increasingly complex work. Third, supplement with external specialist support for specific categories or initiatives where internal capability does not yet exist. This is where a firm like Trace adds the most value: providing senior procurement practitioners who can execute immediately while building internal capability alongside the existing team.

Governance: The Invisible Architecture

Governance is the element of the operating model that gets the least attention in design and causes the most friction in operation. It covers three things: decision rights, escalation paths, and performance measurement.

Decision rights define who can approve what. At what spend threshold does a category manager have authority to award a contract? When does it escalate to the CPO? To the CFO? To the board? Poorly defined decision rights create bottlenecks (everything escalates because nobody is sure of their authority) or risk (decisions are made without appropriate oversight because the governance framework is unclear).

Escalation paths define how disagreements between procurement and the business are resolved. When a business unit wants to sole-source a supplier and procurement recommends a competitive process, who decides? When a supplier relationship is underperforming but the business unit wants to retain them, who has the final say? Without clear escalation paths, these disagreements become political battles that damage relationships and slow decision-making.

Performance measurement defines what success looks like. If procurement is measured solely on cost savings, the function will optimise for lowest price, potentially at the expense of quality, risk, and supplier sustainability. If procurement is measured on a balanced scorecard that includes savings, supplier performance, contract compliance, risk management, and stakeholder satisfaction, the function will optimise for value. What gets measured gets managed, and the choice of metrics shapes the operating model more powerfully than most organisations realise.

Technology: An Enabler, Not a Strategy

The temptation in any operating model redesign is to lead with technology. Buy a new e-procurement platform, implement a contract management system, deploy a spend analytics tool, and expect the operating model to transform. It does not work that way. Technology amplifies whatever operating model it sits on top of. If the underlying processes are poor, the data is messy, and the team does not have the capability to use the tools, technology investment will deliver expensive disappointment.

The right sequence is: design the operating model first, define the processes, build the capability, then implement the technology that enables and accelerates the model. For most Australian organisations, the technology priorities in a procurement transformation are spend visibility (you cannot manage what you cannot see), contract management (knowing what you have committed to and when it expires), and workflow automation (removing manual processing from routine procurement activities so the team can focus on strategic work).

Getting the Sequencing Right

Procurement transformations fail more often on sequencing and change management than on strategy. The common pattern is: develop an ambitious target operating model, present it to the executive, get approval, and then attempt to implement everything simultaneously. The result is overwhelm, resistance, and regression to the old way of working within six to twelve months.

The approach that works is phased implementation with early wins. Start with spend visibility: consolidate spend data, classify it by category, and present the executive team with a clear picture of what the organisation is spending, with whom, and under what contract arrangements. This step alone often reveals enough opportunity to fund the next phase. Then build category management capability in two or three high-value categories where the opportunity is greatest and the business stakeholders are most receptive. Deliver measurable results in those categories. Use those results to build credibility and mandate for expanding the model across the portfolio.

This takes 12 to 24 months for a mid-sized organisation and 24 to 36 months for a large, complex one. There are no shortcuts. But the compounding effect of each phase building on the last means the function's impact accelerates over time.

How Trace Consultants Can Help

Trace Consultants is an Australian procurement, supply chain, and operations advisory firm. We work with organisations across retail, FMCG, hospitality, infrastructure, government, and defence to design and implement procurement operating models that deliver measurable value.

Operating model design. We work with CPOs and executive teams to design procurement operating models that fit their organisation's size, complexity, maturity, and strategic objectives. Our approach is practical, phased, and grounded in what actually works in Australian organisations, not theoretical frameworks imported from global consulting playbooks. Learn more about our procurement capability.

Category management and sourcing execution. We provide experienced category managers who can execute sourcing events, build category strategies, and deliver results while developing internal capability alongside your team. Explore our procurement services.

Procurement transformation and change management. We support the full lifecycle of procurement transformation: from maturity assessment and target operating model design through to implementation, capability building, and performance measurement. See our project and change management capability.

Organisational design for procurement functions. We help organisations get the structure, roles, and governance right, including the sensitive transition from transactional to strategic operating models that requires careful management of existing teams. Explore our organisational design services.

If your procurement function feels busy but not impactful, the problem is almost certainly in the operating model. The team is not lacking effort. It is lacking the structure, capability, governance, and tools to convert effort into value.

Start with an honest assessment of where you sit on the maturity curve. Map your spend. Identify the categories where the opportunity is greatest. And invest in the capability that will move the function from processing transactions to driving strategic outcomes.

The organisations that treat procurement as a strategic function outperform those that treat it as an administrative one. The operating model is what makes the difference.

Hormuz is the first chokepoint to break. The Malacca Strait, Lombok, and Sunda are next in line. Australia's supply chain strategy needs a geographic reset

Building Northern Resilience: Why Australia's Supply Chain Strategy Needs a Geographic Reset

The Hormuz crisis has focused national attention on a single chokepoint. That is understandable. The closure of the strait has removed roughly 20% of global oil supply from the market, triggered the largest coordinated release of strategic petroleum reserves in history, and pushed Australian fuel prices to record levels. But focusing on Hormuz alone misses the deeper structural lesson.

Australia's fuel security, and its broader supply chain resilience, does not depend on one chokepoint. It depends on a chain of maritime chokepoints stretching from the Persian Gulf through the Indian Ocean to the Indonesian archipelago. The Strait of Hormuz. The Strait of Malacca. The Lombok Strait. The Sunda Strait. These waterways carry the vast majority of Australia's maritime trade: roughly 83% of imports and 90% of exports transit through Southeast Asian sea lanes.

Hormuz is the first link in that chain to break. The question that government, defence, and infrastructure leaders should be asking is not "how do we respond to this crisis?" It is "what happens if the next disruption is closer to home?"

This article examines the layered geographic vulnerability of Australia's supply chains, the case for a deliberate northward shift in resilience infrastructure, and the practical supply chain planning that government, defence, and critical infrastructure operators should be undertaking now.

The Chain of Chokepoints: Australia's Layered Vulnerability

The standard framing of Australia's fuel vulnerability focuses on import dependency: Australia imports roughly 90% of its refined fuel, has only two operating refineries, and holds reserves well below the International Energy Agency's 90-day standard. All of that is true, and all of it matters. But it is only the first layer.

The second layer is the refinery dependency. Australia does not import crude from the Gulf in significant volumes. It imports refined products from Asian refineries in Singapore, South Korea, and China. Those refineries depend on Gulf crude. So the Hormuz disruption hits Australia indirectly, through the refining system that sits between the Gulf and Australian fuel terminals. That creates a lag (the subject of the first article in this series) but it also creates a concentration risk: a small number of refining hubs, located in a small number of countries, processing crude from a single dominant supply region.

The third layer, and the one that has received the least attention, is the geographic corridor through which refined products reach Australia. Every tanker, container ship, and bulk carrier arriving at an Australian port from Asia transits through the narrow waterways of Southeast Asia. The Malacca Strait is 1.5 miles wide at its narrowest point and carries the highest concentration of commercial shipping of any waterway on earth. The Lombok and Sunda straits are the primary alternatives, but they are not wide-open ocean: they are defined corridors with their own navigational constraints and geopolitical contexts.

If a disruption in the Middle East were to coincide with, or trigger, disruption in Southeast Asian sea lanes, whether through state-level coercion, grey-zone activity, piracy escalation, or broader regional conflict, Australia would not simply face expensive fuel. It would face physically constrained access to refined products, containerised goods, and industrial inputs. The rerouting options are limited: sailing around Australia's south adds days to every voyage and does not solve the problem of constrained origin-end loading.

This is not a theoretical scenario. The 2023 Defence Strategic Review warned explicitly that Australia's assumed strategic warning time had eroded. The current crisis is demonstrating in real time how quickly maritime disruption can cascade through supply chains. The lesson is that resilience planning needs to account for disruption at any point along the maritime corridor, not just at the most distant chokepoint.

The Case for a Northern Shift

Australia's current fuel and supply chain infrastructure is concentrated in the south and east. The two operating refineries are in Brisbane and Geelong. The major fuel import terminals are in Sydney, Melbourne, Brisbane, and Fremantle. The national fuel distribution network is designed to flow product from these coastal terminals inward by road and rail.

This configuration works when the supply chain is functioning normally. It is structurally vulnerable when it is not. If imports through Southeast Asian sea lanes are constrained, southern and eastern terminals are the last to receive supply, because they are the furthest from the origin of inbound shipping. Northern Australian ports, by contrast, are geographically closer to alternative supply corridors and to the Pacific routes that bypass Southeast Asian chokepoints entirely.

ASPI has argued that the centre of gravity in Australia's fuel security debate must shift north. The logic is straightforward: distributed fuel resilience requires storage, terminal capacity, and distribution infrastructure positioned across the continent, not concentrated in the population centres of the southeast. Larger northern storage facilities, greater redundancy in import terminals, and expanded capacity to move fuel across the continent during disruption would all materially improve Australia's ability to sustain operations under constrained supply.

This is not solely a fuel argument. The same geographic logic applies to defence logistics, critical mineral processing, food distribution, and industrial supply chains. Northern Australia is closer to allied staging areas, closer to emerging Indo-Pacific trade corridors, and better positioned to receive supply from diversified sources (including the United States, which is now shipping emergency fuel to Australia on 55 to 60-day voyages from the Gulf Coast). Infrastructure investment in the north serves multiple strategic objectives simultaneously: fuel security, defence readiness, economic development, and supply chain diversification.

What Government Agencies Should Be Doing Now

The National Fuel Security Plan agreed by National Cabinet on 30 March 2026 addresses the immediate crisis: emergency reserve releases, fuel quality standard relaxation, Export Finance Australia underwriting for additional cargoes, and a national fuel supply taskforce. These are necessary short-term measures. But the crisis has exposed structural weaknesses that short-term measures cannot fix.

Rethinking strategic reserves

Australia uses more energy from diesel alone than from electricity. Yet the country has failed to meet the IEA's 90-day reserve requirement since 2012. Current reserves of approximately 30 to 39 days provide a narrow buffer that is adequate for short disruptions but wholly inadequate for a sustained closure measured in months. The Hormuz crisis should accelerate investment in the Boosting Australia's Diesel Storage Programme and expand its scope to include northern and remote storage facilities capable of supporting defence, mining, and agricultural operations during prolonged disruption.

Building distributed terminal capacity

The current fuel distribution model relies on a small number of major import terminals. If any of those terminals becomes inaccessible (due to disruption, infrastructure failure, or capacity saturation during a supply surge), there is limited redundancy. Investment in additional terminal capacity, particularly in northern Australia and along the western coast, would provide alternative entry points for fuel imports and reduce the concentration risk inherent in the current network.

Mapping n-tier supply chain dependencies

Government procurement frameworks typically manage direct supplier relationships. The Hormuz crisis has demonstrated that the critical vulnerabilities often sit two or three tiers upstream: the refinery that processes the crude, the shipping line that carries the cargo, the insurance market that underwrites the voyage. Government agencies need to build n-tier supply chain maps for critical categories (fuel, fertiliser, medical supplies, defence materiel, food distribution) that identify chokepoint dependencies and concentration risks across the entire supply chain, not just the direct contract.

Fixing procurement contract frameworks

As discussed in earlier articles in this series, many government procurement contracts lack effective fuel escalation mechanisms, or contain no provision for cost escalation beyond annual CPI review. This is a structural weakness that predates the current crisis but is now causing real operational consequences: suppliers absorbing cost increases they cannot sustain, which will eventually lead to service degradation, variation claims, or supplier failure. The crisis should trigger a systematic review of procurement contract templates across Commonwealth and state agencies, with specific attention to fuel and energy cost escalation, force majeure provisions, and change-in-law clauses linked to the Liquid Fuel Emergency Act.

Integrating fuel security into defence logistics planning

The Australian Defence Force's fuel requirements are significant and operationally critical. The current crisis has reinforced the case for accelerating defence-grade energy systems that reduce reliance on imported petroleum, including synthetic fuels, hybrid energy systems for bases, and distributed fuel storage positioned for operational flexibility rather than peacetime efficiency. Defence logistics planning must assume that fuel supply disruption is a feature of the operating environment, not an exceptional event.

What Critical Infrastructure Operators Should Be Doing

Airports, ports, hospitals, water utilities, telecommunications networks, and energy generators all depend on liquid fuel, whether for primary operations, backup power, or logistics. The Hormuz crisis is a stress test for their supply chain resilience, and the results should inform investment decisions for the next decade.

Audit your fuel supply agreements. Do you have a direct supply agreement with a major fuel distributor that provides priority allocation during constrained supply? Or are you purchasing on the spot market, where you will be lowest priority in a rationing scenario? The difference matters enormously when supply tightens.

Test your backup power assumptions. Many critical facilities rely on diesel generators for backup power. The assumption is that fuel will be available to run them. In a sustained supply disruption, that assumption may not hold. What is your generator runtime at current fuel stocks? What is your resupply plan if fuel deliveries are delayed by days or weeks?

Map your logistics dependencies. Every item that arrives at your facility by truck carries a diesel cost. In a rationing scenario, your suppliers' ability to deliver may be constrained before your own operations are directly affected. Understanding which suppliers operate their own fleets (and have fuel security) versus those that rely on third-party logistics (and are more vulnerable to rationing) is critical planning information.

Stress-test your continuity plans against the current scenario. Most business continuity plans model short-duration disruptions: a 48-hour power outage, a one-week supply interruption. The Hormuz crisis is a multi-month event with uncertain duration. Does your continuity plan account for sustained cost escalation, supplier financial distress, and potential rationing of a critical input? If not, it needs to be updated.

The Longer View: From Crisis Response to Structural Resilience

Australia's geographic advantage, the vast distance that insulates it from most conflicts, has been treated as a substitute for resilience rather than a means of building it. The Lowy Institute has argued that comfort has diluted discipline: because supply chain dependency did not produce a lasting crisis during COVID, it was treated as acceptable. The current crisis is making the costs of that complacency visible.

The structural reforms required are not new ideas. Fuel reserve expansion, domestic refining support, distributed storage, northern infrastructure investment, procurement framework modernisation, and defence logistics transformation have all been discussed in policy circles for years. What the Hormuz crisis provides is the forcing function: the real-world demonstration that these investments are not theoretical hedges against improbable scenarios, but operational necessities for a country that imports 90% of its refined fuel through a chain of contested maritime corridors.

Every oil shock in modern history has generated a proportional policy response. The 1973 embargo accelerated France's nuclear programme. The 1979 Iranian Revolution drove Japan's energy efficiency transformation. The question for Australia in 2026 is whether this crisis will be the catalyst for genuine structural investment in supply chain resilience, or whether, as has happened before, the urgency will fade once prices moderate and the tankers start flowing again.

The organisations and agencies that use this moment to build resilience, not just respond to the crisis, will be the ones best positioned for whatever comes next. And something will come next. The geography of risk has not changed. Only the awareness of it has.

How Trace Consultants Can Help

Trace Consultants works with government agencies, defence organisations, and critical infrastructure operators across Australia on supply chain strategy, procurement, and operational resilience.

Supply chain resilience and risk assessment. We help organisations map their end-to-end supply chain dependencies, identify chokepoint risks and concentration vulnerabilities, and design resilience strategies that balance cost, service, and risk across the network. Explore our strategy and network design capability.

Government procurement advisory. We work with Commonwealth and state agencies on procurement framework design, contract structure review, and category management for critical supply categories. The current crisis is surfacing structural weaknesses in government procurement that require expert attention. See our government and defence sector page.

Defence and national security supply chain planning. We support defence logistics planning, sustainment supply chain design, and scenario modelling for contested supply environments. Our team brings deep experience in defence procurement and operational logistics. Learn more about our government and defence work.

Critical infrastructure supply chain review. For airports, ports, hospitals, and utilities, we provide rapid supply chain vulnerability assessments that identify fuel, logistics, and supplier dependencies and recommend practical resilience improvements. See our planning and operations capability.

The Hormuz crisis will end. The maritime geography that makes Australia vulnerable will not. The chain of chokepoints from the Persian Gulf to the Indonesian archipelago will remain, and the question of whether Australia has the distributed infrastructure, diversified supply corridors, and resilient procurement frameworks to withstand disruption at any point along that chain will persist long after oil prices moderate.

The time to invest in structural resilience is when the cost of not doing so is fresh in memory. That time is now.

Scenario Planning for CFOs: How to Stress-Test Your Procurement Spend in a $100+ Oil World

Most procurement portfolios in Australia were structured, priced, and contracted in a world where Brent crude sat between $70 and $85 per barrel. That world ended on 28 February 2026.

With the Strait of Hormuz effectively closed and oil prices fluctuating between $100 and $120 per barrel, every contract with a fuel, energy, transport, or commodity input component is being repriced, whether the contract anticipated it or not. The question for CFOs and Chief Procurement Officers is not whether their cost base is increasing. It is how much, where, and what they can do about it before the full impact lands.

This article provides a practical, step-by-step framework for stress-testing your procurement portfolio under sustained elevated oil prices. It is designed to be executed in days, not months, and to give executive teams the visibility they need to make informed decisions about contract management, supplier engagement, and budget reforecasting.

Why Procurement Portfolios Are More Exposed Than Most CFOs Realise

The direct cost of fuel and energy is visible and well understood. What is less visible is how deeply oil prices are embedded in the cost structure of almost every procurement category. A CFO looking at their fuel line item sees one number. But oil prices flow into freight rates, packaging costs, chemical inputs, bitumen, plastics, steel production energy costs, fertiliser, food ingredients, and dozens of other categories that are priced against energy-linked indices or cost structures.

In a $75 oil world, these embedded costs are stable and predictable. In a $100+ oil world, they are all moving simultaneously, but at different speeds and with different lag times. That creates a compounding effect that is easy to underestimate when each category is managed in isolation.

The second source of hidden exposure is contractual. Many procurement contracts include mechanisms designed to manage cost volatility: fuel escalation clauses, CPI adjustments, provisional sums, and rise-and-fall provisions. But these mechanisms vary enormously in design, responsiveness, and effectiveness. Some are well-constructed and activate automatically as benchmarks move. Others are poorly drafted, ambiguous, or reference indices that do not reflect actual cost movements. And a significant proportion of contracts, particularly in government procurement, contain no escalation mechanism at all.

In a period of rapid cost escalation, the gap between contracts with effective protection and contracts without it becomes the single largest driver of unbudgeted cost exposure. Identifying that gap is the first priority.

The Five-Step Stress Test

Step 1: Build Your Exposure Map

Start with your top 30 to 50 contracts by annual spend. For each contract, classify the primary cost driver into one of five categories:

Direct fuel and energy. Contracts where fuel or electricity is the primary input cost: fleet management, freight and logistics, equipment hire, generator supply, aviation.

Transport-intensive. Contracts where the goods or services delivered have a high transport cost component relative to total value: building materials, bulk commodities, food distribution, waste management.

Commodity-linked. Contracts where the input materials are priced against commodity indices that correlate with oil: bitumen, plastics, chemicals, steel, aluminium, packaging.

Labour-intensive with fuel exposure. Contracts where the supplier's cost base includes significant vehicle fleet or equipment fuel costs: cleaning, landscaping, security (mobile patrols), facilities maintenance.

Low exposure. Contracts where the primary cost driver is labour, software, professional services, or other inputs with minimal direct oil price sensitivity.

This classification does not need to be precise. It needs to be directionally correct. The goal is to separate your portfolio into high, medium, and low exposure tiers so that effort is focused where it matters.

Step 2: Audit Your Contractual Protection

For every contract in the high and medium exposure tiers, answer four questions:

Does the contract include a fuel or energy escalation clause? If yes, what index does it reference? How frequently does it adjust? Is the adjustment automatic or does it require a claim or negotiation? Is there a cap or collar?

Does the contract include a CPI adjustment? CPI adjustments provide some protection, but they lag actual cost movements by quarters, not weeks. In a rapid escalation, CPI clauses undercompensate in the short term. They are better than nothing, but they are not a substitute for a fuel-specific mechanism.

Does the contract include rise-and-fall or provisional sum provisions? These are common in construction and infrastructure contracts. The critical questions are whether the provisions are broadly enough drafted to capture fuel-linked cost increases, and whether the adjustment mechanism is responsive enough to track the pace of current movements.

Does the contract include a force majeure clause that could be triggered? The Hormuz closure and potential government-imposed fuel rationing raise legitimate force majeure questions. If the Australian government invokes the Liquid Fuel Emergency Act and imposes allocation controls, that is a new legal requirement post-dating most existing contracts. Many change-in-law clauses extend to subordinate legislation and government directions that affect a contractor's ability to perform or increase its costs. Legal analysis of these provisions should be underway now, not after rationing is announced.

For each contract, the audit produces a simple assessment: protected, partially protected, or unprotected. The unprotected contracts in high-exposure categories are your immediate priority.

Step 3: Model Three Price Scenarios

Build a simple scenario model using three oil price assumptions across a 6-month horizon (April to September 2026):

Scenario A: Resolution by mid-year. Brent crude returns to $85 to $90 by July. Diesel prices in Australia settle at 15 to 20% above pre-crisis levels. Freight surcharges moderate but do not fully unwind. Commodity input costs stabilise. Total additional procurement cost: 3 to 6% above baseline for high-exposure categories.

Scenario B: Prolonged disruption. Brent crude remains at $100 to $120 through September. Diesel prices stabilise at 30 to 40% above pre-crisis levels. Freight surcharges persist at 15 to 20%. Commodity inputs remain elevated. Supplier cost claims arrive across all major categories. Total additional procurement cost: 8 to 15% above baseline for high-exposure categories.

Scenario C: Escalation. Brent crude spikes to $140+ as strategic reserves are depleted and the conflict escalates. Diesel rationing is introduced in Australia, prioritising defence, emergency services, and agriculture. Commercial construction, logistics, and mining face supply curtailment. Total additional procurement cost: 15 to 25% above baseline for high-exposure categories, with material risk of project delays and supplier failure.

For each scenario, multiply the estimated percentage increase against the annual spend in each exposure tier. This gives you a total cost impact range that can be reported to the board and used to reforecast budgets.

The precision matters less than the discipline. A model that is directionally correct and available this week is infinitely more valuable than a precise model that arrives in June.

Step 4: Identify Decision Triggers and Response Levers

For each scenario, define the specific conditions that would trigger a management response, and the response itself.

Contract renegotiation triggers. At what cost level does an unprotected contract become material enough to warrant renegotiation? What is the contractual mechanism for reopening pricing: a scheduled review, a variation, a force majeure claim? Who needs to approve the renegotiation, and what is the lead time?

Supplier engagement triggers. At what point do you proactively engage your top 10 suppliers to understand their cost exposure and discuss collaborative responses? The answer should be "now", but the framework should define what that engagement looks like: a structured cost review, a shared scenario model, a joint identification of cost reduction levers.

Budget reforecast triggers. At what cost impact level does the procurement function need to formally reforecast and escalate to the CFO and board? Define the threshold (for example, a projected 5% increase in total addressable procurement spend) and the reporting format.

Project deferral or scope reduction triggers. For capital projects, at what cost escalation level does the business case need to be revisited? What projects could be deferred, rephased, or descoped to manage the budget impact? What is the cost of delay versus the cost of proceeding at elevated input prices?

Supplier failure early warning. Which of your critical suppliers operate on thin margins and are most vulnerable to a sustained cost increase they cannot pass through? What are the early indicators of financial distress (late deliveries, quality issues, delayed invoicing, unusual payment requests)? What is your contingency if a critical supplier exits the market?

Step 5: Execute the Engagement Plan

With the exposure map, contractual audit, scenario model, and decision triggers in place, the execution priorities become clear:

Week 1. Complete the exposure map and contractual audit for your top 30 contracts. Brief the CFO and executive team on the preliminary findings.

Week 2. Complete the scenario model. Identify the five to ten contracts with the largest unprotected exposure. Initiate supplier engagement for those contracts.

Week 3. Begin contract renegotiation or variation processes where required. Submit budget reforecast if the projected impact exceeds the defined threshold. Brief the board on the overall risk position and management response.

Ongoing. Update the scenario model fortnightly as market conditions evolve. Track supplier cost claims against the model to validate or challenge claim quantum. Monitor early warning indicators for supplier financial distress across the critical supplier base.

Common Gaps We See in Australian Procurement Portfolios

Having worked across procurement functions in retail, FMCG, hospitality, infrastructure, and government, there are several patterns that consistently create disproportionate exposure in a crisis like this.

Fuel escalation clauses that reference the wrong index. A clause tied to the Singapore Gasoil benchmark will produce a different outcome from one tied to the AIP Terminal Gate Price for diesel. In a volatile market, the basis risk between indices can be significant. Many contracts reference an index chosen for convenience rather than accuracy.

CPI adjustments treated as a substitute for fuel escalation. CPI movements lag fuel price movements by months. In a stable environment, the difference is immaterial. In the current environment, a contract relying solely on CPI adjustment is effectively unprotected for the first two to three quarters of the crisis.

Government contracts with no escalation mechanism at all. This is disturbingly common in Australian government procurement. Many panel arrangements, standing offer deeds, and period contracts were tendered and priced in a low-volatility environment with no provision for cost escalation beyond annual CPI review. Suppliers to government are absorbing cost increases they cannot pass through, which will eventually result in service degradation, variation claims, or supplier withdrawal.

Freight contracts with outdated fuel levy structures. Many shippers are running fuel levy mechanisms that were designed for a $70 to $85 oil environment and are not calibrated for the pace and scale of current movements. The lag between actual fuel cost and recovered levy is creating cashflow pressure for carriers and cost uncertainty for shippers.

No visibility over tier-two supplier exposure. Your direct supplier may have a reasonable cost structure, but if their key input supplier is exposed to Middle Eastern energy costs, that exposure will eventually flow through. Procurement functions that only manage direct supplier relationships have a blind spot that this crisis will exploit.

Minimum volume commitments in a demand-constrained environment. Some procurement contracts include minimum volume or take-or-pay commitments that were set during normal operating conditions. If diesel rationing forces production curtailment or project delays, organisations may find themselves contractually obligated to purchase volumes they cannot use, or paying penalties for shortfalls. These clauses need to be reviewed against downside scenarios now, not after a rationing order is issued.

Preparing for Rationing: The Scenario Most Procurement Teams Have Not Modelled

The Liquid Fuel Emergency Act 1984 has not been invoked as of early April 2026, but the government has publicly modelled scenarios involving 10%, 30%, and 50% supply reductions over 30-day periods. For procurement teams, the rationing scenario introduces a qualitatively different challenge: it is not just about cost, it is about physical availability.

Under the National Liquid Fuel Emergency Response Plan, priority allocation goes to defence, emergency services, hospitals, and food production. Commercial construction, logistics, manufacturing, and mining sit in lower priority tiers. That means a formal rationing regime could restrict your suppliers' ability to operate, deliver, or fulfil contracted obligations, regardless of price.

The procurement response to a rationing scenario has several dimensions. First, review whether government-imposed rationing constitutes a force majeure event under your key contracts, and whether change-in-law clauses would be triggered by a Ministerial direction under the Liquid Fuel Emergency Act. Second, understand which of your critical suppliers have direct fuel supply agreements with major distributors (giving them some security of allocation) versus those buying on the spot market (who would be first to lose access). Third, identify which activities you would defer, descope, or pause under each rationing tier, and pre-agree those decisions with internal stakeholders so they can be executed quickly if required.

The organisations that have done this planning in advance will respond to a rationing announcement with a structured operational adjustment. Those that have not will respond with ad hoc crisis management, which is always more expensive and more disruptive.

How Trace Consultants Can Help

Trace Consultants is a specialist supply chain, procurement, and operations advisory firm that works with Australian organisations across retail, FMCG, hospitality, infrastructure, government, and defence. We bring practical procurement expertise and deep sector knowledge to every engagement.

Procurement portfolio stress-testing. We build rapid scenario models that map your fuel, energy, and commodity cost exposure across your entire procurement portfolio, identify contractual gaps, and quantify the financial impact under multiple price scenarios. Our models are designed to be iterated as conditions change and to provide CFOs and boards with the decision-quality information they need. Learn more about our procurement capability.

Contract review and renegotiation. We work alongside your procurement team to audit fuel escalation mechanisms, benchmark contracted rates against current market pricing, and structure renegotiations that protect your position while maintaining critical supply relationships. For government clients, we bring deep understanding of Commonwealth and state procurement frameworks and the specific contractual challenges they create. Explore our procurement services.

Supply chain resilience and strategy. For organisations looking beyond the immediate crisis to build structural resilience into their supply chain and procurement operating model, we provide end-to-end strategy and implementation support. See our strategy and network design capability.

Government and defence advisory. We work with federal and state government agencies on procurement policy, supply chain risk, and operational resilience. The current crisis is surfacing structural weaknesses in government procurement frameworks that require urgent attention. See our government and defence sector page.

The procurement portfolio stress-test described in this article can be started today and completed within two to three weeks. It does not require new systems, new data, or new processes. It requires a structured approach, clear prioritisation, and the discipline to act on what the analysis reveals.

The organisations that will manage this period most effectively are those that know their exposure, have modelled the scenarios, and have defined their decision triggers before the next wave of cost pressure arrives.

Your procurement portfolio was built for a different world. The world has changed. The question is whether your response has changed with it.

Most boardrooms are focused on fuel prices. The bigger shock is coming through fertiliser shortages, food input inflation, and compounding freight surcharges.

Fertiliser, Food, and Freight: The Second-Order Supply Chain Shock Most Australian Executives Aren't Planning For

The headlines are about petrol prices. The boardroom conversations are about diesel. But the supply chain shock that will define Q3 and Q4 2026 for Australian retailers, food service operators, FMCG businesses, and agriculture is not the fuel crisis itself. It is the second and third-order effects that are still working their way through the system: fertiliser shortages, agricultural input cost inflation, and the compounding effect of elevated freight surcharges on every link in the food supply chain.

These effects operate on longer lag times than fuel prices. They are harder to see in real time. And for most Australian executives outside the agricultural sector, they are not yet on the radar. That is a problem, because by the time they show up in supplier cost claims and category P&Ls, the window for proactive response has already closed.

This article traces the physical mechanics of the fertiliser and food supply chain disruption, maps the timeline of impact for Australian businesses, and provides a practical framework for modelling the cost exposure before it arrives.

The Fertiliser Crisis: Bigger Than Most People Realise

The Strait of Hormuz is not just an oil chokepoint. It is a fertiliser chokepoint. Roughly 20 to 30% of globally traded fertiliser, including urea, ammonia, phosphates, and sulphur, normally transits through the strait. The Persian Gulf is the world's dominant production region for nitrogen-based fertilisers, with Saudi Arabia, the UAE, and Qatar supplying approximately 42% of Australia's total fertiliser import value in 2024.

Australia consumed 8.7 million tonnes of fertiliser in 2024, valued at A$5.5 billion. Of that, 7.9 million tonnes were imported. Domestic production is negligible: Australia's only urea manufacturing facility (Incitec Pivot's Gibson Island plant) closed in 2022, and the planned Perdaman facility in Western Australia will not be operational until mid-2027 at the earliest. Australia's largest ammonia plant has also been shut for maintenance during the crisis.

The numbers tell the story. Urea, which accounts for 44% of Australia's fertiliser consumption, has surged from around A$850 per tonne in late February to over A$1,400 per tonne in recent weeks: an increase of more than 60%. Nearly a million tonnes of fertiliser cargo are physically stranded in the Gulf. Fertilizer Australia, the sector's peak body, has warned the government that further shipping disruptions would have "catastrophic impacts on domestic agricultural output in the 2026 season."

Unlike oil, there are no internationally coordinated strategic reserves for fertiliser. No government stockpile to release. No emergency mechanism to bridge the gap. When fertiliser supply is disrupted, the only responses are to source from alternative origins (at higher cost and longer lead times), reduce application rates (accepting lower crop yields), or defer planting entirely.

Why the Timing Is Critical for Australia

The Hormuz closure could not have come at a worse time for Australian agriculture. Winter grain crops are typically sown between April and June. Most growers had secured 70 to 80% of their planting fertiliser (primarily MAP and DAP) before the crisis, but supplies of post-planting nitrogen inputs, specifically urea and urea ammonium nitrate, are now critically short.

This distinction matters. Planting fertiliser goes into the ground at sowing. Nitrogen top-up is applied during the growing season to drive protein content and yield. Without adequate nitrogen, crops still grow, but yields and quality fall materially. For wheat, the difference between a well-fertilised crop and an under-fertilised one can be 20 to 30% in yield and a downgrade from milling quality to feed quality, which carries a significant price penalty.

Industry analysts estimate Australia's wheat plantings could drop 10 to 12% this year, with further reductions in canola, which is a nitrogen-hungry crop. Some growers are shifting to less fertiliser-intensive crops like barley and pulses. Others, particularly those carrying high debt or coming off years of drought, may choose not to plant at all.

The ripple effects are significant. Australia is the world's fourth-largest wheat exporter. A material reduction in planted area or yield does not just affect individual farm economics. It reduces national export volumes, tightens domestic supply, and contributes to upward pressure on global grain prices at a time when Northern Hemisphere production is facing the same fertiliser constraints.

Tracing the Cost Transmission Into Food and Grocery

For executives in retail, FMCG, and food services, the question is: when and how does this show up in my cost base? The answer requires tracing three parallel cost transmission pathways, each with a different timeline.

Pathway 1: Freight surcharges (already arriving)

Every product that moves by truck, rail, or ship carries a fuel cost component. With diesel up 30 to 50% and major freight operators flagging 15 to 20% surcharge increases, this is the first and most visible cost impact. It is already flowing through to distribution centre operations, store deliveries, and last-mile logistics. For a national grocery chain or FMCG distributor, freight typically represents 3 to 8% of cost of goods sold. A 15 to 20% increase in freight costs adds 0.5 to 1.5 percentage points to total COGS, which is material on thin retail margins.

Timeline: immediate to 4 weeks.

Pathway 2: Supplier cost claims on materials and packaging (arriving now through May)

Packaging materials (plastics, glass, cardboard, aluminium) carry significant embedded energy costs. So do processing and manufacturing inputs. Suppliers who absorb these increases for a few weeks will eventually pass them through as formal cost claims to their retail and food service customers. The lag depends on contract structures, supplier cashflow resilience, and the pace of raw material inventory turnover.

Most FMCG and grocery suppliers operate on 60 to 90-day cost review cycles. Claims filed in April and May will reference cost increases accumulated since early March. The scale of individual claims will vary, but procurement teams should expect a broad-based wave of cost increase requests across categories with high energy, transport, or packaging input cost weightings.

This is the slow-burn pathway, and the one least visible to most executives today. Fertiliser costs are flowing into planting decisions right now. Those decisions will determine yield outcomes in the second half of the year. At the same time, on-farm fuel and chemical costs are rising, increasing the farm-gate cost of production for everything from grain and oilseeds to vegetables, dairy, and livestock feed.

The transmission mechanism is not instant. Grain harvested in Q4 2026 was planted in Q2 at higher input cost. Livestock producers feeding that grain face higher costs through the second half. Dairy and meat production costs rise accordingly. Fresh produce growers facing both fertiliser and fuel cost increases are already reducing planting schedules: half of Australian vegetable growers have reported they will run out of fertiliser within three weeks, and 27% have already cut production.

For grocery retailers and food service operators, this means farm-gate price increases on fresh produce, dairy, grain-based products, and meat that begin arriving in Q3 and persist into Q4. Food price inflation of 4 to 8% above baseline is a credible central estimate, with higher outcomes possible if the crisis extends and Northern Hemisphere production is also affected.

Timeline: 12 to 24 weeks.

The Compounding Effect: When All Three Pathways Converge

The critical insight for supply chain and procurement leaders is that these three pathways do not operate in isolation. They compound.

A product that costs more to grow (fertiliser), more to process (energy), more to package (materials), and more to deliver (freight) accumulates cost increases at every stage. A loaf of bread, for example, carries the cost of wheat (fertiliser and fuel-dependent), milling (energy-dependent), packaging (materials-dependent), and distribution (diesel-dependent). Each input has increased, and the cumulative effect is larger than any single line item suggests.

For a category manager looking at a supplier cost claim in June, the challenge is separating out how much of the claimed increase is driven by genuine input cost escalation versus opportunistic margin recovery. That requires granular visibility into the cost structure: what proportion of the product's cost is transport, what proportion is raw material, what proportion is energy, and how each of those has moved since the crisis began.

Organisations with mature should-cost models, clean input cost indices, and established supplier engagement processes will be able to validate claims quickly and negotiate from a position of knowledge. Those without that capability face a binary choice: accept claims at face value (and overpay), or reject them across the board (and risk supplier exits or service degradation at a time when alternative supply is scarce).

What This Means for Specific Sectors

Grocery and Supermarkets

National grocery chains face cost pressure across virtually every category simultaneously. Fresh produce (fuel and fertiliser), dairy (feed costs and energy), bakery (wheat and energy), packaged goods (materials and freight), and chilled/frozen (cold chain energy costs) are all exposed. The cumulative effect across a full-range supermarket could be a 3 to 6% increase in cost of goods sold by Q3, which translates to hundreds of millions of dollars annually for a major chain.

The strategic procurement response is to prioritise early engagement with key suppliers on a category-by-category basis, validate cost claims against independently sourced input cost data, and identify categories where substitution, reformulation, or specification changes could mitigate the impact.

FMCG and Packaged Goods

FMCG manufacturers face a margin squeeze between rising input costs and retailer resistance to shelf price increases. The pressure is greatest in categories with high raw material content (cleaning products, personal care, packaged food) and high transport intensity (beverages, bulky goods). Manufacturers with strong brands and limited private label competition have more pricing power. Those in commoditised categories face the hardest trade-off between margin and volume.

Food Services and Hospitality

Hotels, integrated resorts, quick-service restaurants, and contract caterers face a particularly acute version of the problem. Food and beverage cost structures are being compressed from above (input cost inflation) and below (consumer resistance to menu price increases in a cost-of-living environment). Unlike grocery retail, where price adjustments can be made weekly, many hospitality operators work with quarterly or seasonal menus, contracted rates for events and conferencing, and brand standards that limit substitution.

The scenario modelling priority is to stress-test the F&B P&L under a 15 to 25% increase in combined food and energy input costs over two quarters. For a large hospitality operator with $50 to $100 million in annual F&B procurement, the exposure is $7.5 to $25 million. Menu engineering, supplier rationalisation, waste reduction, and procurement process improvement become urgent operational levers, not long-term optimisation projects.

Agriculture

Farmers are the first link in the chain and the most exposed to both cost increases and physical supply constraints. Grain growers are making planting decisions right now with incomplete information about fertiliser availability and price. Livestock producers are watching feed costs rise and making stocking decisions that will affect production volumes for months. Vegetable growers are already cutting production schedules.

The farm-level response to high input costs has a direct downstream impact on every business that relies on agricultural output. Reduced plantings mean tighter supply. Tighter supply means higher prices. Higher prices mean more cost pressure on everyone from supermarkets to food manufacturers to restaurant operators.

A Practical Modelling Framework for Executives

Step 1: Map your food and agricultural input cost exposure

Identify which products and categories in your business have significant exposure to agricultural inputs, packaging materials, energy, and freight. Rank them by spend and by sensitivity to input cost changes. Focus on the top 15 to 20 categories that account for the bulk of your cost base.

Step 2: Build a timeline of expected cost impacts

Use the three-pathway framework above to map when cost increases are likely to arrive for each category. Freight surcharges are here now. Supplier cost claims on materials and packaging will peak in April to June. Agricultural input cost inflation will arrive in Q3. Overlay these timelines to understand the cumulative impact across your portfolio.

Step 3: Model three cost scenarios across a 6-month horizon

Scenario A (resolution by May): freight surcharges moderate, supplier claims are manageable, agricultural impact is limited. Total COGS increase: 2 to 4%.Scenario B (crisis extends through Q3): freight remains elevated, supplier claims accelerate, farm-gate prices rise materially. Total COGS increase: 5 to 8%.Scenario C (prolonged disruption into Q4): compounding effects across all three pathways, potential physical shortages in some categories. Total COGS increase: 8 to 12%.

Step 4: Identify your response levers

For each scenario, define the actions available: supplier renegotiation, specification changes, menu or range engineering, alternative sourcing, inventory buffer adjustments, and pricing pass-through. Quantify the impact of each lever and sequence them by speed of implementation and scale of effect.

Step 5: Engage suppliers before claims arrive

The organisations that engage suppliers proactively, with a clear framework for cost validation and a collaborative approach to shared problem-solving, will get better outcomes than those that wait for claims to land and then react defensively. Understanding your suppliers' own exposure to the same pressures is the foundation for a negotiation that protects both parties.

How Trace Consultants Can Help

Trace Consultants works with Australian retailers, FMCG businesses, hospitality operators, and food service organisations to build practical, data-driven responses to supply chain cost pressure. Our team brings deep procurement expertise and sector-specific operational knowledge to every engagement.

Procurement cost modelling and scenario analysis. We build rapid scenario models that map your food, packaging, energy, and freight cost exposure across your procurement portfolio, identify the categories most at risk, and quantify the financial impact under multiple disruption scenarios. Learn more about our procurement capability.

Supplier engagement and cost validation. We work alongside your procurement team to prepare for and respond to supplier cost claims, using independently sourced input cost data and should-cost modelling to separate genuine increases from margin recovery. Explore our procurement services.

F&B and back-of-house optimisation. For hospitality and food service operators, we help design procurement operating models, centralised ordering systems, and cost-of-goods frameworks that provide real-time visibility over input costs and margin performance. See our BOH logistics capability.

Supply chain strategy for retail and FMCG. From network design to inventory policy to supplier diversification, we help organisations build supply chains that are resilient to sustained cost pressure and supply disruption. Explore our strategy and network design services.

The second-order supply chain shock from the Hormuz crisis is not speculative. The fertiliser is not on the water. The planting decisions are being made right now. The cost transmission pathways are well understood, and the timelines are predictable within reasonable bounds.

The executives who will protect margins and maintain competitive position through the second half of 2026 are those who model the impact now, engage suppliers early, and activate response levers before the cost pressure becomes unavoidable.

The fuel crisis got everyone's attention. The food and fertiliser crisis will determine who navigates 2026 successfully and who doesn't.

Diesel powers 40% of mining, every construction site, and the freight network that moves everything Australians buy. The cost shock is repricing all of it.

Diesel is the Economy: How the Hormuz Crisis is Repricing Australian Supply Chain Cost Models

Diesel is not a line item. It is the economy.

It powers the trucks that deliver every product on every supermarket shelf. It runs the excavators, concrete pumps, and cranes on every construction site in the country. It fuels the haul trucks that move iron ore and coal from pit to port. It keeps cold chains running, waste trucks moving, and hospital backup generators turning over. When diesel prices move, everything moves with them.

In March 2026, diesel climbed above $3 per litre in several Australian capital cities. Terminal gate prices jumped 45 to 50 cents per litre in under two weeks. For a transport operator buying a standard 36,000-litre load, that translates to roughly $18,000 more per delivery than a fortnight earlier. For the mining sector, agriculture, construction, and logistics, the numbers scale accordingly.

This is not a temporary price blip. It is a structural repricing driven by the closure of the Strait of Hormuz, the effective removal of 20% of global oil supply from the market, and the cascading impact on Asian refineries that produce the vast majority of Australia's imported fuel. Diesel is the fuel type most exposed: Australia imports roughly 120,000 barrels per day of diesel from South Korea alone, and alternative supply routes from the US Gulf Coast take 55 to 60 days compared with the usual 7 to 14 from Asia.

For supply chain and procurement leaders, the question is not whether costs are rising. That is obvious. The question is how to model the impact, identify the contracts and cost lines most exposed, and make decisions that protect margin and continuity over the next two to three quarters.

Why Diesel, Specifically, Is the Pressure Point

Not all fuels are equally affected by the Hormuz disruption. Diesel carries disproportionate exposure for three reasons.

First, Australia's diesel deficit is the deepest of any fuel type. Domestic refineries (primarily Ampol's Lytton facility in Brisbane and Viva Energy's Geelong refinery) produce some petrol and jet fuel, but their output skews away from diesel. The gap between domestic diesel demand and domestic diesel production is larger than for any other refined product, making Australia almost entirely dependent on imports for the fuel that underpins its heaviest industries.

Second, diesel demand is structurally inelastic in the short term. A household can defer a weekend drive or combine errands to reduce petrol consumption. A mine cannot stop its haul trucks. A construction site cannot pause concrete pours. A cold chain operator cannot switch off refrigeration. The industries that consume the most diesel are the industries least able to reduce consumption quickly, which means demand holds firm even as prices spike.

Third, diesel is the fuel most likely to be rationed first if the crisis deepens. Defence, emergency services, and agriculture sit at the top of the priority allocation list under Australia's national liquid fuel emergency framework. Commercial construction, logistics, and mining fall below those categories, meaning that in a formal rationing scenario, the sectors that consume the most diesel face the greatest risk of supply curtailment.

Mapping the Cost Transmission: How Diesel Reprices Supply Chains

Diesel cost increases do not sit neatly in one budget line. They transmit through supply chains in layers, each with a different lag time and a different degree of visibility to the organisation paying the bill.

Layer 1: Direct fuel costs (immediate)

Any organisation that operates a vehicle fleet, runs diesel-powered equipment, or maintains backup generation feels this instantly. Fuel is typically the largest or second-largest variable cost for road freight operators, earthmoving contractors, and mining haul operations. A 30 to 50% increase in diesel prices flows through to operating costs within days.

For a mid-sized road freight operator with annual diesel spend of $5 to $10 million, a sustained 40% price increase adds $2 to $4 million per year in direct cost, against industry margins that typically sit between 3 and 7%. That is not a rounding error. It is an existential pressure.

Layer 2: Freight and logistics surcharges (2 to 6 weeks)

Transport contracts almost universally include fuel levy mechanisms, but those mechanisms lag actual costs by two to four weeks and are often calculated against benchmark indices that smooth out short-term volatility. In a rapidly escalating price environment, the gap between actual fuel cost and recovered fuel levy widens, creating cashflow pressure for carriers and cost uncertainty for shippers. Major freight operators including Toll, Linfox, and StarTrack have already flagged surcharge increases, and businesses across Australia are reporting 15 to 20% hikes in logistics costs.

Layer 3: Embedded energy in materials and inputs (4 to 12 weeks)

Steel, cement, glass, aluminium, and plastics all carry significant embedded energy costs. When diesel and broader energy prices rise, production costs for these materials increase, and those increases flow through to buyers with a lag of one to three months depending on contract structures and inventory buffers. The Housing Industry Association has warned that sustained fuel price increases could add $8,000 to $15,000 to the cost of building a new home, driven largely by the embedded energy cost of materials and the cost of transporting them to site.

Layer 4: Input cost inflation in agriculture and food (8 to 20 weeks)